|

In Frank Norris' novel The Octopus one of the characters says: "Our century is about done. The great word of

this nineteenth century has been production. The great word of the twentieth century will be-listen to me, you

youngsters-markets."

The statistics certainly confirm the dominance of production in nineteenth-century America. In 1860 about

$1,000,000,000 was invested in manufacturing; by 1900 the figure was almost $10,000,000,000. In the same period the

value of manufactured goods rose from almost $2,000,000,000 to $13,000,000,000. In that year before the Civil War began,

the total national wealth, as best it can be estimated, was $16,000,000,000; in thirty years it increased to

$65,000,000,000, and then in the next ten years it jumped to $88,500,000,000. While the population doubled between 1860

and 1890, the number of persons employed in industry increased nearly three times. The amount of horsepower used

increased four times.

Before the war the United States had been an agricultural nation, although industry was growing steadily. By 1890 the

value of manufactured goods exceeded that of agricultural products, and in just another ten years was double the value

of farm products. The number of people engaged in industry now outnumbered those in agriculture, and in 1894 America

became the largest producer of industrial products in the world.

A number of factors contributed to this phenomenal growth. First of all, the Civil War had stimulated industrial

enterprise, especially in the North, and the accompanying inflation had further encouraged expansion. But there were

more basic reasons. The most important of these was that the nation was blessed with great natural resources of soil,

water and minerals. The supply of labor grew regularly both from a natural increase of the population and as a result of

immigration. The protective tariff system that grew up during the Civil War stimulated the growth of certain industries.

As time went on, American manufacturers and merchants were increasingly able to sell goods abroad, while at the same

time the domestic market expanded with the population. A surge of practical inventions and new technology made a

distinct contribution. Finally, the railroad network tied the nation together and made it possible to move raw materials

and finished products over a continent, while the expansion of the railroad lines was in itself one of the greatest

stimulants to industry.

The new industrial era brought changes other than the quantitative one of more goods produced. It revolutionized the

economic life of the nation, threatened the political structure and brought about a confrontation between capital and

labor, rich and poor, that more than once resulted in bloodshed. Factories became larger, business organizations became

more complex. Out of this grew the trend toward the corporate form which, by the end of the century became the dominant

form of business organization. The legal entity that was the corporation made it possible to gather the large capital

funds necessary for modern business, and to spread the risk among hundreds or thousands instead of a few partners. This

process also resulted in more efficient and scientific management of the complex industrial system.

As the corporations grew in size and separated employers from employees, new social and political, as well as economic,

problems arose. How could the individual laborer get economic justice from a large corporation? How could the general

public protect itself, as a group of citizens and consumers, front the power of the men who monopolized a whole

industry? And what was this new system, this new power and wealth, doing to the men at the top who benefited the most

from it?

Nowhere were such questions more relevant than in the iron and oil industries, and nowhere else had a combination of

skill and good luck led to such achievements in production and such accumulations of fortune. The iron and steel

factories developed the industrial muscles that enabled the United States to become the giant of the new industrial age.

Iron had been smelted since colonial days but steel, a more difficult and expensive product, was just beginning to be

commercially important at the end of the Civil War. The spectacular growth of steel production during the remainder of

the century rested on several strong, foundation stones. One was technological-the development of new processes

utilizing chemistry and electricity. The Bessemer process, named for an Englishman, Henry Bessemer, was the first step.

It made the production of steel more efficient and less expensive. Based on the oxidation of impurities in iron, and

using less coal, the process was first applied in this country about 1865. In the 1880's the open-hearth process took

steel production a step further. Lower-grade iron ores could be used and the high quality of the steel could be

maintained at a uniform level.

The United States outdid the rest of the world in the practical application of these new techniques, but there were

other reasons why the country took the lead. New ore fields with enormous resources were discovered in the Lake Superior

region; and one, the Mesabi Range, became the greatest ore producer in the world. The Mesabi fields had the added

advantage that the ore was near the surface, requiring no underground mining, and was free of impurities that would have

interfered with the steel-making, process. By a combination of water and rail transportation, this ore and the needed

coal and other raw materials were brought together at comparatively small cost. On top of this, the industry was able to

convince Congress that a high tariff on iron and steel imports was necessary to protect the "Infant" American industry

from foreign competition. Despite the tariff, the prices of iron and steel products showed a steady downward trend with

some fluctuations due to supply and demand. The fortunes of the steel industry were also closely tied to those of the

railroads, and until the late 1880's rails were the most important product of the steel mills. The railroads also used

iron and steel for locomotives and cars, and, as the techniques for building with steel instead of wood were developed,

for railroad bridges. In the latter part of the century, the production of steel for the construction of buildings also

became important.

The figures for the last third of the nineteenth century tell the story. In 1867 only 20,000 tons of steel were

produced in America, but by 1900 production was 10,000,000 tons and American production had passed that of Great Britain

by 1895. Pig-iron production by 1900 was up to more than 13,000,000 tons, and the mining of coal (much of it processed

into coke) kept pace. By the end of the century the value of iron and steel production was about $800,000,000-four times

what it had been thirty years earlier. In this same period the number of workers employed in the industry increased from

about 77,500 to 222,500, and the amount of capital invested from $121,772,000 to $513,392,000. When the twentieth

century arrived, the United States was producing more steel than Great Britain and Germany combined.

Beyond technology, natural resources and the protective tariff, the United States possessed another asset that had a

great deal to do with its industrial achievements. That asset consisted of intelligent, hard-working men, each of whom

desired to be rich, to be powerful to produce and to outsmart competitors. The outstanding leader of this type in the

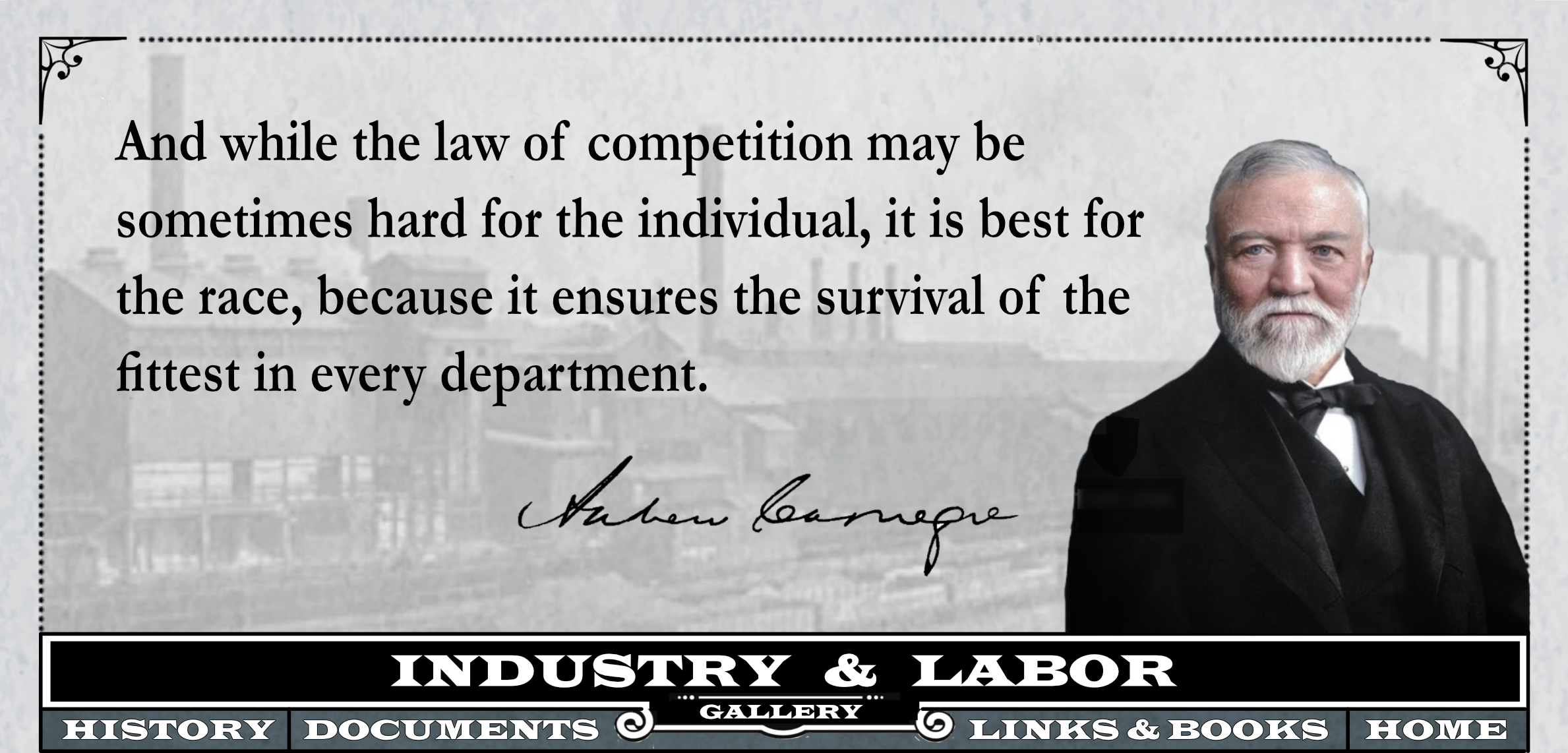

steel industry, and one of the top industrialists of all fields, was Andrew Carnegie (1835-1919). Carnegie, the son of a

poor weaver, was born in Scotland and was brought to the United States by his family in 1848. The family settled in

Pittsburgh and in 1849 Carnegie went to work as a messenger for a telegraph company. He soon became a telegraph

operator, then caught the attention of an executive of the Pennsylvania Railroad, and succeeded him as superintendent of

a division. At the start of the Civil War Carnegie helped the Federal government organize its military railroad and

telegraph facilities, but he did not serve in the armed forces.

Carnegie had already been investing in business enterprises. He saw the possibilities in manufacturing railroad

sleeping cars and steel bridges. At the same time he was getting more and more involved in the iron and steel business

in Pittsburgh, and shortly decided to concentrate his interests and efforts in that field. As he said: "Put all your

eggs in one basket, and then watch that basket." He also said: "Whatever I engage in I must push inordinately." The

principle and the attribute both worked well for Andrew Carnegie. He was reputed to be a millionaire by the time he was

thirty, and by 1873 he was acquiring other iron works. In 1875 he built the Edgar Thomson Steel Works, the most modern

facility of its kind in the world. He hired able men and had capable partners, although none so determined and daring as

himself. He was a tough competitor who cut prices when he thought he could take business away from others, who fought

continually with the railroads to get better freight rates, and who entered pools and agreements when it served his

purpose and dropped out when it was to his interest to do so.

Most of all, though, Carnegie achieved his paramount position in the industry because he was always discarding old

machinery and processes for new ones. He ploughed back into the business far more of the profits than most of his

partners liked. He was not interested just in the annual dollar profit he could achieve, but in the amount of steel and

iron he could produce, in the volume of business he could secure, in the efficiency of his machines and his employees.

By the 1890's he had made his company into a vertically integrated corporation that had its own sources of iron ore and

coal, its own railroads and shipping, its own plants for making crude iron and steel, and its own fabricating machinery

for turning iron and steel into a variety of finished products. By 1900 his plants were turning out about a quarter of

all the steel produced in the United States. The next year, when America's first billion-dollar corporation, the United

States Steel Company, was formed, Carnegie received about a quarter of a billion dollars (in 5 per cent gold bonds) for

his share of the business he had started little more than a quarter century earlier.

The oil industry, which did not exist until 1859, grew even more spectacularly than the iron and steel industry.

Petroleum, coming to the surface in small quantities of its own accord, had been known for centuries, and in America had

been associated with the Native Americans, who used it medicinally. As Indian oil or Seneca oil, it had been sold as a

cure-all for diseases of man and beast. When in 1859 Colonel Edwin L. Drake, on Oil Creek in Pennsylvania, drilled a

well and produced a large, steady flow of crude oil, a new industry was born. Soon the oil region of western

Pennsylvania and southwestern New York resembled the California gold rush area of a decade earlier. Anyone with a little

money, a lot of energy and the willingness to take a risk could drill a well.

There was great demand for the oil, its primary use for many years being in the form of kerosene for lighting. It

replaced whale oil and candles, and American kerosene was soon sold all over the world. There were, though, a number of

technological and financial problems involved. Hundreds of independent producers had their own few wells. This crude oil

had to be transported from many scattered sources, in hills and wooded areas, to refineries. Oil refining was in its

infancy and the methods and machinery were constantly being changed and improved. Even refineries in the early days were

small and numerous. Finally, the finished products had to be distributed by rail and ship, and sold in competition with

other refiners. In 1860, 500,000 barrels of crude oil were pumped out of the ground, by 1900, annual production was

nearly 60,000,000 barrels. As early as 1865 the United States was exporting $16,000,000 worth of petroleum products,

giving the industry sixth place in rank in foreign trade, and the figure grew as the years went on.

In the early years of the oil boom there were as many as 1,100 different companies producing or refining petroleum-or

at least selling stock in their concerns. By the end of the century about 85 percent of the oil industry-some

authorities thought the figure even higher-was under the control of one organization, the Standard Oil Company. The man

primarily responsible for creating this near-monopoly, and who dominated the oil industry as Carnegie stood foremost in

steel, was John D. Rockefeller (1839-1937). Thrifty and industrious, Rockefeller began his career at the age of sixteen

as a bookkeeper in Cleveland, Ohio. Within five years he became a partner in a produce commission business. In 1863 he

joined with some other men to build an oil refinery in Cleveland, then a center of the industry.

This group made steady progress toward its goal of controlling the whole industry. The Rockefeller interests bought

out other refineries as cheaply as possible. They did--not try to purchase oil wells, but rather to control the

transportation of the crude oil and to be the largest purchasers so that they could set their own price in competition

with the numerous, individualistic and unorganized producers. They built their own pipelines and made secret

arrangements with railroads, promising the roads a large volume of business if they were given lower freight rates than

their competitors. At times they even received from the roads some of the freight charges paid by competing oil

companies. At the wholesale and retail end of the business, Standard Oil deliberately sold its products at a loss when a

dealer handled a rival's products, until such time as the dealer gave up. Then Standard's prices went back up.

Rockefeller and his colleagues did not owe all their success to sharp practices and ruthless competition. They operated

the most efficient refineries and were ever on the lookout for new techniques. Standard Oil found it was cheaper to make

its own wooden barrels, and on at least one occasion Rockefeller himself chided a manager for being unable to account

for 500 of the small pieces of wood used as bungs in the barrels.

Standard Oil also led the way in the legal manipulation of business organization, and the example it set was followed

in other industries and businesses. Standard formed the first large trust in 1882. In this scheme the stockholders of

forty oil companies turned over their stock to nine trustees. They received trust certificates in return, and the

trustees ran all the firms as one business instead of forty firms competing with each other. The Ohio courts broke up

this scheme in 1890, but in 1899 the Rockefeller interests found an even better system. Under lenient laws in New Jersey

they formed a corporation that was to be a holding company-it owned the stock of other companies as well as operating

itself. By 1900 the assets of Standard Oil Company of New Jersey were over $200,000,000.

Through all these years Rockefeller lived austerely, giving large sums to his church, saying very little in public,

but becoming some-thing of an ogre, compared with Andrew Carnegie, in the eyes of the people. There was a widely held

opinion that Standard Oil would do anything in the way of bribery and unfair competition to sell its products and force

its competitors out of business. Yet its products were good, and in general the prices of petroleum products declined.

Rockefeller never doubted his own goals and good intentions, but he did say once: "Work by day and worry by night, week

in and week out, month after month. If I had foreseen the future I doubt whether I would have had the courage to go

on."

The story in other areas of economic life was much the same, although without such paramount figures as Carnegie and

Rockefeller. In mining, in meat packing, in textiles, as well as in other fields, great discoveries were made,

technologies advanced, and hard-driving men made fortunes never before imagined. Mining was not new but it was only in

the second half of the century that the overwhelming riches beneath the nation's soil were revealed. Mining not only

became a leading industry by itself, but it also underlay the expansion of the iron and steel industry and the

railroads, while at the same time it provided the precious metals that formed the basis of the monetary system.

Except for coal in Pennsylvania and iron ore in the Lake Superior region, mining was mainly an industry of the Far

West. In fact, the lure of sudden riches, by bringing thousands of people into the area west of the Mississippi, was a

major factor in the general settlement of the region and the eventual disappearance of the frontier. The discovery of

the Comstock Lode in Nevada was the most spectacular event of its kind. This, the richest silver deposit ever found, was

first mined in 1859. Virginia City, founded that same year, had a population Of 35,000 in the 1870's and was the chief

mining town of the whole West. Between 1860 and 1890 the Comstock Lode yielded $340,000,000 worth of silver, but by the

end of the century it was practically worked out and abandoned.

Gold and silver were found in Colorado, too, while Montana was revealed to be rich in copper deposits. In 1896 word

came back to the states that gold had been discovered in the Klondike region of Alaska, and by 1898, 30,000 adventurers

had gone to the icy north to seek their fortunes. Between 1860 and 1890, men dug out of western lands $1,242,000,000

worth of gold and $901,000,000 worth of silver. The effect of the flow of this wealth was felt not only in the economic

field, but also in politics when the question of hard money versus soft, and bimetalism versus the gold standard became

for a time the leading issue.

The meat packing industry, which grew so rapidly that for a while the value of its products was greater than that of

any other industry, owed its expansion to several factors. The Civil War stimulated it with the necessity of feeding the

large Union armies. At the same time, population was increasing. Ranchers began operating in the great plains west of

the Mississippi River, and the railroads pushed westward to provide transportation for the livestock. Thus, like mining,

the meat packing industry contributed to the settlement of the continent and the passing of the frontier.

The problem, then, was to bring the products of the farms and ranches from the West to the East, where the large

population created a profitable market. At mid-century, Cincinnati, Ohio, was the leading center of meat packing, but

during the war Chicago, Illinois, took the lead and held it. Among the leaders of Chicago's packing industry were Philip

D. Armour (1832-1901) and Gustavus F. Swift (1839-1903). Both were excellent organizers, creating nationwide systems for

slaughtering, processing, distributing and selling. Swift pioneered in developing refrigerated railroad cars which made

it possible to sell fresh meat products all over the country. The mechanized techniques used in meat processing were

forerunners of the modern factory assembly line. A joke of the time said that in Armour's plant no part of a pig was

wasted except the squeal. Armour and Swift joined with two other leading packers to keep down the prices they paid for

livestock, and they bullied the railroads, in the manner of Standard Oil, to get preferential rates. In the course of

their efforts to lower costs and increase profits, the packers were often accused of having very low standards of

sanitation in their plants. No laws existed to protect consumers, and without question the packers were careless and

contemptuous of public opinion. Tainted meat and canned meat with foreign substances in it reached the public and it was

not until the early years of the twentieth century that anything was done about it.

While the North and the West were prospering, the South was struggling to recover from the ravages of the Civil War.

The large plantations were broken up and tenant farming became the accepted form for much of the agricultural life of

the region. The railroad system had been badly damaged during the war and it was many years before it was restored and

expanded. Gradually the South recovered, and in the process it became less an agricultural region and followed to some

extent the trend of industrialization. Coal and iron in Tennessee and Alabama laid the foundations for a southern iron

and steel industry of considerable consequence after 1880. Lumbering became an important business and by 1890 the

southern states were the chief suppliers to the nation. Tobacco growing and manufacturing became a large industry.

It was in textiles, however, that the South made the most noticeable advance. Before the war most of the cotton town

in the South was sent to Great Britain or New England to be made into cloth. In the last two decades of the century,

more and more of the manufacturing was done locally. In 1880 there were 161 mills in the South, but by 1900 there were

400, and they were spinning more than half the cotton in the country. New plants were built in the South; sometimes

under local sponsorship, sometimes by New England mill owners who found labor costs and taxes much lower in the South.

Nearness to the supply of raw materials was another factor in attracting mills to the region. An entire cotton mill was

moved from New England to the South for the first time in 1889.

To build railroads, steel mills, mining machinery, textile mills and other industrial equipment required a great deal

of money in the form of capital to be invested. Business and industrial units became so large that individuals and even

partnerships could not provide the necessary funds. The corporate form of organization became attractive because

corporations could sell stocks and bonds to hundreds or thousands of people and institutions. Selling the stocks and

bonds required the services of investment bankers and the trading system of stock exchanges. Much European capital,

especially from Great Britain, flowed into the United States, although the country was increasingly able to supply its

own capital needs. The bankers and financiers, who invested their own funds and recommended investment opportunities to

others, became essential to industry, and they began to exercise considerable influence over it. They took seats on

boards of directors to watch over the capital for which they were responsible. Their interest in making a profit on

invested capital sometimes was at odds with those whose chief interest was in producing goods.

By far the foremost banker and financier of the period was J. Pierpont Morgan (1837-1913). Although the family was

American, Morgan's father ran a successful investment firm in London. The younger Morgan took over the family interests

and made the American office the most important firm of its kind. Morgan's first great interest was in railroads, where

he labored to merge individual lines into larger, regional units. At one time it was estimated that the House of Morgan

exercised some sort of control over nearly half the railroad mileage of the country. Morgan's relations with the large

insurance companies gave him access to huge funds whose investment he could control. His greatest single coup was

putting together the United States Steel Corporation. This project also demonstrated his love of order in business. He

wanted the steel industry, for example, to be stable and strong enough to set its own terms.

In person Morgan matched his banking philosophy. Piercing eyes and an enormous red nose (which no one dared comment

on made him a forbidding figure. He was imperious, curt and decisive, and he easily dominated other men because he

always seemed so sure as to exactly what should be done. He was of course wealthy beyond count and used his money for

many purposes. His yacht was the largest private yacht of all. He was an active lay leader in the Episcopal Church and

delighted in taking Bishops to church conventions in his private railroad car. His collection of paintings, rare books

and other valuable objects was his greatest interest. His son gave what had been the elder Morgan's home and library to

the public in 1924.

Quite another type of person, but also typical of financiers of the era, was Jay Gould (1836-1892). Starting as a

clerk, he quickly began to make money by various speculations and, in the course of his life, he made and lost millions.

Undistinguished in appearance and mean in spirit, he never had any interest in improving the operations of a railroad,

but he delighted in securing control of a road, such as the Erie, by devious and unfair means. He then manipulated its

stocks and bonds until he could squeeze nothing more out of the road. At one time or another he controlled various

railroads, the Western Union Telegraph Company, New York City's steam driven railroads, and a newspaper, the New York

World. Morgan was awesome, and not exactly loved by the man in the street, but Gould was widely disliked, even by his

fellow speculators, and became a leading symbol of the autocratic and selfish business leaders of the period on whom

many people blamed their economic troubles.

The growth of American industry, business and finance yielded many benefits. The national wealth increased. Better

products were produced more efficiently and the prices of many of them decreased. Generally, wages increased during the

period in relation to the cost of living. But as the factories grew larger, and as these larger factories were merged

into even larger corporate units, the dangers and disadvantages of such a trend began to appear along with the

advantages. Small businesses were squeezed out of existence at a time when many Americans still felt there was virtue in

small business just because it was small. The larger the business, the more power it had to corrupt or at least to

influence government officials. The fiercer the fight for markets and profits, the more a business was tempted to use

its economic power to make questionable deals with railroads and its suppliers. Most of all, many people believed that

the men at the top reaped a disproportionate share of the wealth produced, and that the little man at the bottom was not

getting his share.

Opposition to the trend industry was taking gradually became widespread and vocal, and was centered about two hated

words: trust and monopoly. Farmers, wage earners, consumers and reformers took up the cry that government must step in

and regulate big business in the public interest. To them, a trust was any large concern that dominated, or seemed to

dominate, its field of enterprise; although, strictly speaking, the trust form of organization was giving way to the

corporation and the holding company. A trust, it was assumed, used its position to overcharge the consumer, underpay the

worker, and pocket enormous profits for the owners and the bankers. Large profits were certainly made, some by efficient

production, good management and successful sales efforts, but a great deal of money was also made by men who produced

nothing except merger deals and new issues of stocks to speculate in.

Mergers increased: there were eighty-six combinations in the decade ending in 1897, but 149 in the next three years

alone. As the mergers continued and the new millionaires began flaunting their wealth, public opinion became aroused and

an antitrust crusade with a moral fervor behind it began in the 1880's. Standard Oil was pointed at as the worst

monopoly of all, but there were---or were alleged to be-trusts with monopolistic power in many fields. There were the

Distillers and Cattle Feeders' Trust, the American Sugar Refineries Company, and, supposedly, monopolies in wall paper,

shoe laces and schoolbooks. The Oatmeal Trust was said to have closed some of its mills, putting many men out of work,

and then, as demand outran the artificially restricted supply, to have raised the price of oatmeal $1.00 a barrel.

By the late '80's public opinion was such that political leaders of both parties realized something must be done to

appease the people, although the Republican party and the controlling elements of the Democratic party were inclined to

side with big business. Those few who could look at the problem objectively sought to regulate business enough to

protect the public without hurting the efficiency and productivity of modern industrialism. The law that came out of

Congress and was signed by President Harrison was, however, vague, although it sounded firm and ferocious. The first

section of the Sherman Anti-Trust Act of 1890 declared:

Every contract, combination in the form of trust or otherwise, or conspiracy, in restraint of trade or commerce among

the several states, or with foreign nations, is hereby declared to be illegal...

The law proved ineffective in dealing with the misdeeds of the trusts. In the first decade of the law's existence the

government brought only eighteen court actions tinder it. Moreover, the Supreme Court interpreted the law so as to

render it almost harmless to the monopolists. The most important case before 1900 was that concerning the Sugar Trust.

The court decided in 1895 that even though the trust controlled the manufacture of 95 per cent of the refined sugar

produced in the United States, it was not violating the Sherman Act because manufacturing itself was not interstate

commerce.

Retail trade experienced the same kind of growth as did manufacturing: new techniques, population growth, nationwide

transportation and communication all led to expansion. In 1870 about 850,000 persons were engaged in trade, finance and

real estate; by 1900 this number had grown to 2,870,000. And as in manufacturing, this growth spelled the doom of

thousands of small, individually owned businesses. Department stores which offered almost everything under one roof were

one manifestation of the trend. In a way they were just larger country general stores, and they grew out of the

operation of dry goods stores. As they became bigger along with the cities they did business in, they made millionaires

of so-me of the pioneers. Alexander T. Stewart opened such a store in New York in the 1860's. In Philadelphia, John

Wanamaker (who later bought out Stewart) started his emporium in 1877. In 1881 Marshall Field founded in Chicago what

became one of the largest of all.

Selling by mail became possible as the railroads and the express services spread, and it was further stimulated when

the Post Office Department instituted Rural Free Delivery in 1896. Montgomery Ward and Company was founded in 1872 and

by the 1890's offered 24,000 items in its catalog. It boasted from the start that it could save its customers money by

selling goods directly from the manufacturer. Richard Warren Sears began his career by selling watches by mail. He soon

branched out and Sears, Roebuck and Company was organized in 1893. The next year it issued a 322-page catalog with a

cover printed in color, and gave its customers a money-back guarantee. In the meantime the third notable change in

retailing took place with the advent of the chain stores operating over the whole country, or through large regions. The

Great Atlantic and Pacific Tea Company started in 1858; by 1870 it operated eleven stores and by 1880, one hundred. The

F. W. Woolworth chain that sold all items for five or ten cents opened its first unit in Pennsylvania in 1879, and by

the mid-'90's had twenty-eight stores. Others followed. Mail-order selling and chain-store systems aroused the

antagonism of small-town merchants, who were often supported by local newspapers. The public, however, voted for the new

order of business by patronizing the catalogs and the chain stores so that they grew steadily.

America's exports and imports showed tremendous increases in theGilded Age. The nation produced for export

agricultural products, metals from the mines and finished goods. Over the period exports expanded more than imports and

in most years exceeded the latter, which consisted of raw materials, luxury goods and items not produced at home, such

as rubber and coffee. In 1870 the nation sold abroad about $455,200,000 worth of goods; in 1900 the figure was

$1,370,700,000. Imports increased from $453,958,000 in 1870 to $789,310,000 in 1900. Although the total value of

agricultural goods exported continued to increase as more and more farms produced larger crops, manufactured goods began

to account for a larger proportion of exports: farm products were 79 percent of exports in 1870 and 61 percent in 1900,

while manufactured goods went up from 15 percent to nearly 32 percent. There was some increase, too, in the share of

foreign trade with the nations of Africa and Asia. The pervasive influence of American missionaries in these lands was

one important reason for this increase.

The business and industrial expansion was not one continuous boom. It had its shocks and setbacks. In September,

1873, the most prestigious investment banking house in the nation, Jay Cooke and Company, closed its doors and admitted

it could not meet its obligations. Brokerage houses failed, railroads went bankrupt and the New York Stock Exchange

closed down. This ended an era of overoptimism and excessive railroad construction which had tied up large amounts of

capital but was not profitable. For six years after 1873 there was little railroad building, and as many as 3,000,000

people were unemployed. Prices dropped almost 30 per cent. Immigration decreased. Gradually the depression wore itself

out, aided in 1879 by good crops in the United States at a time when crops were poor in Europe. This in turn led to a

boom in railroad traffic and the economy turned upward again.

Much the same thing happened in 1893. Agriculture had been depressed for several years, with the price of cotton in

the South only about half what it had been ten years before. Since the earlier recovery railroad expansion had again

gone too far, and mostly on credit. When a large London investment banking house collapsed, a financial panic was

triggered. European interests withdrew invested capital from the United States. When railroads again went into

bankruptcy and the steel industry declined, the banking system, poorly organized for serving the new industrialism,

could not stand the strain. By December, 1893, 600 banks had closed their doors. By the following June, 194 railroads

had failed, and in the winter of 1893-94 the chief sufferers, the unemployed, numbered around 2,500,000. In the

meantime, Republicans blamed the depression on people's fears of the Democrats, whose Grover Cleveland entered the White

House in March, 1893, favoring a lower tariff. Democrats blamed the depression on the large government spending and the

high tariff of the Republicans. Advocates of the gold standard blamed the agitation for more and cheaper money. The

silverites and Populists blamed it all on the gold standard and the alleged shortage of currency in circulation. Except

for agriculture, the low point of the depression came in 1894. Gradually times got better, and good times could safely

be said to have come back in 1897 when the European demand for wheat was almost twice what it had been the year before.

Prosperous European countries also stepped up their purchases of American manufactured goods, sending gold into the

country. By then the railroads needed repairs and new equipment.

Throughout the Gilded Age, the fairly steady increase in the production of all kinds of goods depended more and more

on technology, the application of science and invention to agriculture, industry and business. At the start, the

"practical men" dominated, men who had little or no scientific or academic background but devised improved machinery out

of their own experience. Engineering was just becoming an academic discipline in 1880, and specialization was

increasing. Systematic research for a particular goal, and research organized as part of a business enterprise were not

as yet important. On the whole, inventions were the products of individuals who worked for their own ends, aided by

other individuals eager to promote a gadget or an idea. The invention and the use of new machinery and processes were

growing. In 1860 the Patent Office granted 4,363 patents; by 1900 the annual total was over 22,000. Along with the

greater use of science and its practical products went a belief that this represented progress, and that man was

achieving control over nature. It was taken for granted that man could control the machines he was devising.

New inventions and techniques involved not only large industrial processes, such as steel making, but also an endless

variety of items that could be used in homes and offices as well as factories. The leading example, perhaps, is the

typewriter, which was commercially usable in the late 1870's. By 1890 thirty factories were producing them, and the

machine was largely responsible for bringing women into the business world. Cheaper paper, the mass production of

pencils and the invention of the fountain pen all spurred communication. So did the invention of the typesetting machine

the linotype-together with larger and faster presses. Adding machines and cash registers speeded business transactions.

A forerunner of a still more mechanized future was Herman Hollerith's machine which tabulated punched cards. It was

used, very successfully, in the 1890 United States Census.

As significant as such developments were, the fundamental area in which technology was most needed, and in which it

achieved its most spectacular results, was in the conversion of new sources of energy into power-power that was

relatively cheap, reliable, and usable in large and small amounts. At the beginning of the Gilded Age steam power ruled.

The steam engine's efficiency was steadily being improved, but it had its drawbacks: it could not be stopped and started

readily; it could not be made in small easily transportable units. A number of inventors saw the internal combustion

engine as a possible solution, and by 1876 an improved one was on the market. By 1900 about 200,000 were in use around

the world, burning gas rather than a liquid fuel. The internal combustion engine did not come fully into its own until

early in the next century when its superiority as a power plant for vehicles was demonstrated.

The source of energy and power that best filled the new needs turned out to be electricity. Electricity was first put

to practical use in communications equipment-the telegraph and the telephone. Then its possibilities for illumination

began to be explored, and by 1879 the carbon arc lamp was used successfully for lighting streets and other large open

areas. A mile of New York's Broadway became a "great white way" in 1880. In illumination, electricity began to replace

gas, in spite of improvements such as the Welsbach mantle of 1890. The electric motor was being improved at the same

time, although it was not until the 1890's that the alternating current induction motor became widely used. By 1900

electric motors were producing 300,000 horsepower. Electric motors proved much more flexible for industrial use than the

large steam engine. They could be produced in many sizes and each machine in a factory could have its own power source

that could be turned on and off at will. Late in the century the water power of Niagara Falls had been successfully

transformed into alternating electric current, and in November, 1896, the current was transmitted over wires from the

Falls to Buffalo, a distance of twenty miles. So much energy had never been sent so far before.

The wizard who more than any other man applied electricity to all kinds of machines and devices was Thomas A. Edison

(1847-1931). Edison was born in Ohio, where he had only a few months of schooling. He first sold newspapers on railroad

trains, then became a telegraph operator. By the time he was thirty he had set up his own laboratory and devised

improvements for telegraph equipment. He invented the phonograph in 1878 and in the next year he produced the first

practical incandescent electric light bulb. Light bulbs and other electrical equipment were of little use, though,

unless some regular, central source of supply could be made available. Edison worked on this problem and in 1882 opened

the Pearl Street Station in New York City, which at the start supplied power for 2,323 lamps. By 1884, as many as 11,272

lamps were connected to this power source. Edison established a plant in Schenectady to manufacture some of the many

items he had invented. When merged with another company in 1892, this firm became the General Electric Company, with

6,000 employees. Almost alone, Edison brought into being the age of electricity in which people everywhere could secure

power and light from a distant central source, just by pushing a button or turning a switch. Edison's well-equipped

laboratory, in which he used a number of assistants, was an invention factory. He knew little of basic science and his

research was that of a practical man seeking to solve a problem.

Many different kinds of men were responsible for transforming the nation in the late nineteenth century into a fully

operating industrial society. They were the organizers, the managers, the bankers, the inventors. They also included the

schemers, the speculators, and the men who wanted money and power no matter what they had to do to get it. The system

that developed had many faults, but it had many accomplishments to its credit. Its leaders did not believe in the rights

of labor, but they provided more and better jobs than were available before. The factory, with its noisy and dangerous

machinery geared to the mass production of thousands of identical objects, provided more conveniences and useful

articles than any other system had ever produced. Mass production did mean uniformity and conformity, but in a democracy

where everyone was in theory the equal of everyone else, this seemed reasonable. Ironically, in the process of providing

look-alike goods for almost the whole population, those who owned and managed the factories made so much money that a

whole class of newly rich arose out of the democratic mass.

It was, indeed, very much the age of the industrial autocrat as well as the age of industrialism. Although such men

as Carnegie, Rockefeller and Morgan came to be called "robber barons," they were admired in many ways, by many people.

The names of business leaders were well known, and they were as much in the public eye as political and military leaders

had been in other times. Most were pious family men, who thought they were by divine will entitled to the wealth they

had helped create. Even those people who formulated reasons for disliking the new men of wealth and power and their

soulless corporations were likely to have a hidden feeling of admiration and awe for these giants of the Gilded Age.

Source: Fon W. Boardman, America and the Gilded Age, 1876-1900

(New York: H. Z. Walck, 1972), 114-126.

|